Workspace spend is out of control.

Access, spend, and policy — governed in one platform.

https://getcroissant.com

Trusted by over 5,000 companies

From access to intelligence,

fully governed.

01 ACCESS INFRASTRUCTURE

Your people are productive anywhere, from day one.

- Space in 100+ cities, available instantly

- Employees book in seconds, not days

- No ops overhead to manage access

WORKSPACES

0+

CITIES

0+

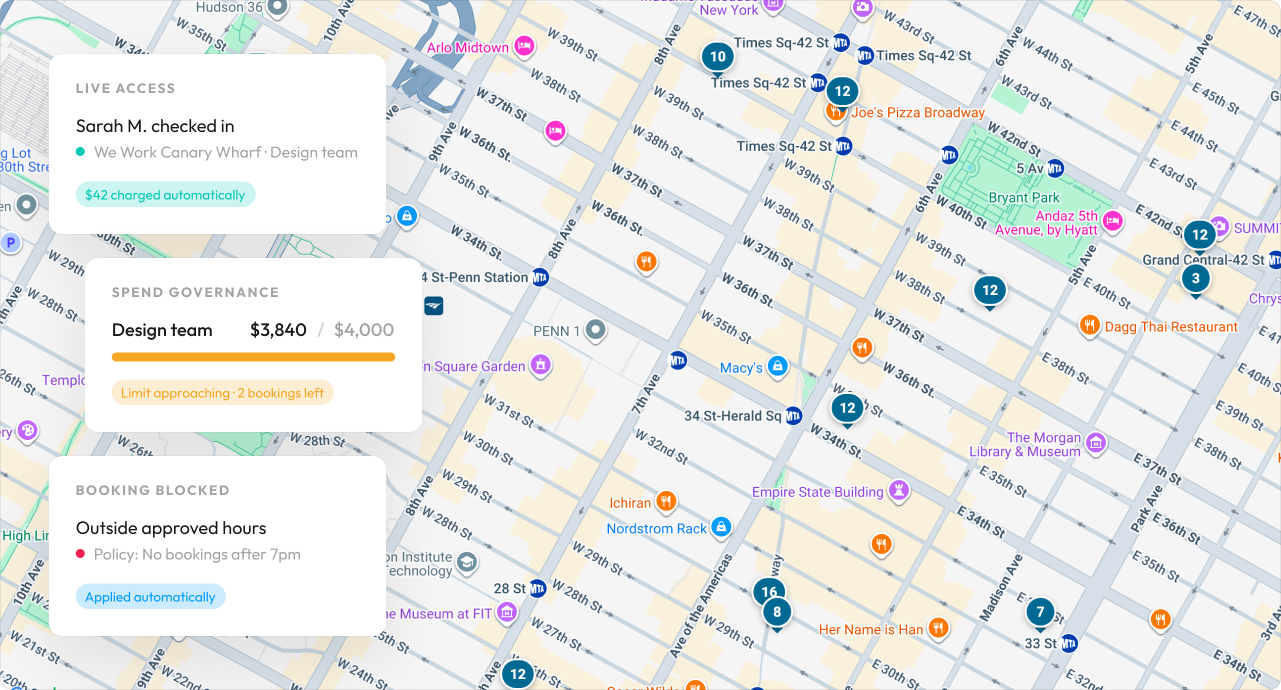

02 WORKSPACE SPEND INFRASTRUCTURE

Every dollar governed. Automatically.

- Budgets set once, enforced everywhere

- Real-time reporting without asking

- Overages blocked before they happen

Engineering

Sales

+4

Design

Operations

Budget cap enforced — Operations

Booking blocked, limit reached. Finance notified.

AVG SPEND REDUCTION

0%

MANUAL APPROVALS

zero

03 POLICY CONTROLS

Set policy once. Enforced everywhere.

- One policy framework, every department, role, and region

- Compliance scales with headcount

- Zero manual enforcement

0%50%100%

0.0%

Compliance rate

Approved workspace types

All regions · All roles

Monthly spend caps

By team · By region

04 VENDOR CONSOLIDATION

One contract. Every workspace.

- One invoice replaces many

- No more juggling vendor relationships across markets

- Vendor relationships governed centrally

THE TRADITIONAL WAY

WeWorkNYC

RegusLDN

IWCBER

SpacesAMS

+9 more contracts

DISTRIBUTED WORKSPACE INFRASTRUCTURE

05 USAGE INTELLIGENCE

See how your team works. Build around it.

- Real-time visibility into where your team works

- High-demand locations surface automatically

- Make real estate decisions backed by actual usage

WORKSPACE UTILIZATION

Tribeca0%

Hudson Square0%

Consolidation opportunity

Tribeca (96%) and Hudson Square (62%) serve overlapping demand. One location could absorb both.

AVG UTILIZATION

0%

LOCATIONS FLAGGED

0

BUILT FOR EVERY STAGE

Workspace that scales with your company, without waste.

Croissant isn't a point solution you replace at 200 employees. The same platform that governs 10 employees governs 1,000+. And every stakeholder sees their value at every stage.

Workspace infrastructure built for early-stage velocity.

- One platform replaces multiple ad-hoc memberships

- Employees get workspace anywhere, instantly

- Budget visibility from day one

60%typically saved vs. a traditional office lease

"Croissant allows us to manage workspace access across regions in a single system, with the flexibility to adjust usage as organizational needs change. It provides visibility, administrative control, and responsive support without adding operational complexity."

Evan DudlaFounder & CTO, Agree

The governance layer growing teams can't afford to skip.

- Spend governed automatically across teams & cities

- Finance gets real-time reporting without asking

- Ops gains control without adding headcount

72%higher satisfaction with flexible workspace access

"Croissant gives our team flexible access to workspaces across cities while keeping everything centralized and easy to manage. As an admin, I value the clear platform overview, the ability to upgrade or downgrade access quickly, and the option to pause when plans change."

Ali HayawiHead of Workplace, Profit Metrics

Global policy, real estate intelligence, and total spend visibility at scale.

- Workspace as a governed, managed asset

- Multi-region policy frameworks enforced globally

- Usage Intelligence informs real estate strategy

2–3%EBITDA improvement within 6 months

"It's the perfect solution because we are a remote-first company. We don't have any offices anywhere and we have people everywhere. Croissant works perfectly because it's something we can offer to everyone."

Júlia Villalba ArandaPeople Operations, Reverse Tech